If there is one topic that is both super important and utterly unsexy, it is pensions in the Netherlands.

Whether you’re an international or not, your pension situation in the Netherlands can have a huge impact on your future income, especially if you don’t end up staying here for 50 years.

Understanding how the system works now means fewer surprises later. It also means more money for your future self, who will hopefully be sipping wine on a terrasje and not worrying about AOW percentages.

So grab a coffee and let’s break down the Dutch pension system.

How the Dutch pension system works

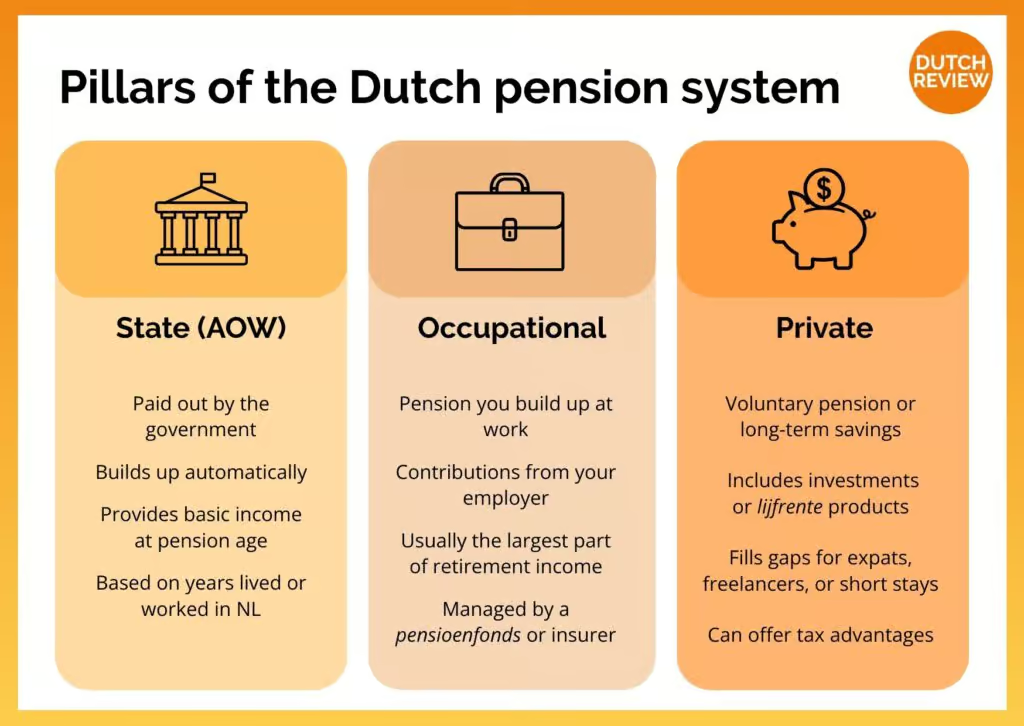

The Netherlands uses a three-pillar pension system. It sounds complicated, but it is one of the more straightforward frameworks in Europe once you unpack it.

The three pillars are:

- The state pension, known as AOW

- The pension you build up through your employer

- Voluntary pension schemes or long-term savings you arrange yourself

Together, these determine how much money you will receive once you leave the workforce.

Most Dutch residents rely on at least two of these three pillars. For internationals, the mix can vary a lot depending on how long you stay in the Netherlands, what jobs you have, and whether you are employed or self-employed.

Many internationals simply opt to arrange a pension for themselves, through financial services like Brand New Day.

Pillar 1: Dutch state pension (AOW)

What is AOW?

The AOW, or Algemene Ouderdomswet, is the basic state pension provided by the Dutch government. It is paid by the Sociale Verzekeringsbank (SVB) and acts as a financial baseline for everyone who has lived or worked in the Netherlands.

READ MORE | Dutch savings accounts: Best interest rates in the Netherlands in July 2026

Unlike many countries, where your state pension depends on your salary, the Dutch system works on residency. You earn AOW rights simply by being insured under the Dutch social security system, which usually means living or working here legally.

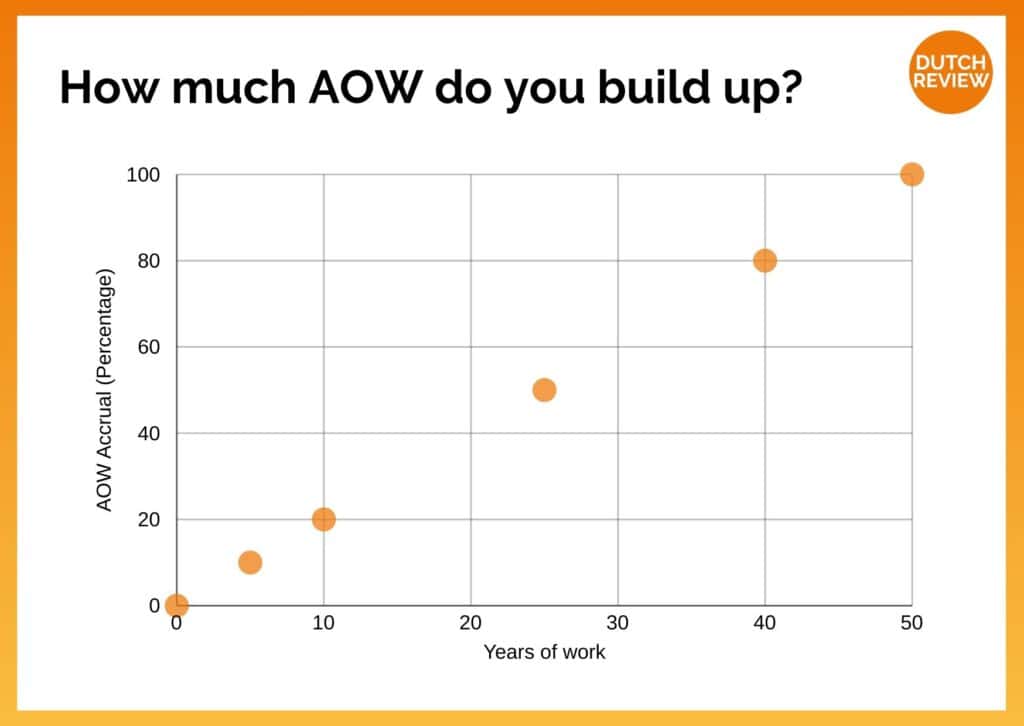

How does AOW accrual work?

Every year you are insured in the Netherlands equals roughly 2% of your total AOW entitlement. You need 50 years of insurance to get the full amount.

A simple example:

- 10 years in the Netherlands means around 20% of full AOW

- 25 years means around 50%

- 40 years means around 80%

This is why internationals often receive a partial AOW unless they stay in the Netherlands for decades.

If you spend years abroad or arrive in the Netherlands later in life, your AOW may be lower. In some specific situations, you may be able to voluntarily insure yourself for missing years, but this depends on age and timing.

When do you receive AOW and how much?

Your AOW age is linked to Dutch life expectancy projections and is calculated based on the day you were born.

This means the retirement age shifts gradually, so always check the most recent update on the SVB website. You can calculate your AOW pension age online.

The amount of your AOW pension depends on your living situation and how many years you were insured under the AOW scheme.

The AOW is designed as a basic minimum income (it roughly follows the statutory minimum wage), so most people need an occupational and/or private pension on top if they want a comfortable retirement.

As of 1 January 2025, a full gross monthly AOW pension for someone living alone is €1,580.92, while partners who both receive AOW each get €1,081.50 gross per month.

These amounts are adjusted twice a year, so always check the latest figures on the SVB site.

Example scenario 1: short stay in the Netherlands (5 years)

Let’s say you live in the Netherlands for five years and then move away. That gives you about 10% of full AOW. You also keep any employer pension you built during those five years.

In retirement, the Netherlands pays your small AOW slice plus any pension fund contributions from your time here.

AOW and expats who leave the Netherlands

If you leave the country before reaching retirement age, you keep whatever AOW percentage you already earned. You do not get it automatically, though. If you live abroad when you reach pension age, you must apply for AOW through the SVB.

Your right to AOW may be affected by the country you move to. Some countries have treaties with the Netherlands, while others do not. Always check early if you plan to retire internationally.

Pillar 2: Occupational pension

If you are employed in the Netherlands, there is a good chance your employer is paying into a pension fund on your behalf.

These pensions are managed by collective funds or insurance companies and usually include both employer and employee contributions.

How do occupational pensions work?

Your Dutch employer often contributes a percentage of your salary to the pension fund each month.

You may contribute as well, depending on the company scheme. Over time, these contributions build up a significant portion of your retirement income.

Occupational pensions are a major part of Dutch retirement planning and often much larger than AOW.

READ MORE | Finding a job in Amsterdam: the ultimate guide in 2026

Not every employer offers a pension plan, though, and some smaller companies do not have one. Always check your employment contract and ask your HR department how your pension is arranged.

What happens if you change jobs?

Because the Netherlands has many pension funds, each job may contribute to a different fund. You can keep pensions from multiple funds without issue.

The Netherlands does not combine them into one pot, but your pension overview tool (more on that below) shows them together.

You can also sometimes transfer pension rights from one fund to another, a process known as value transfer. Whether it is advisable depends on investment performance, fees, and fund health.

Example scenario 2: changing employers several times

Let’s say you work in the Netherlands for 12 years, across three different companies. That earns you about 24% AOW and three small employer pension pots. They may look tiny individually, but together they form a meaningful part of your retirement income.

What happens when you move abroad?

You do not lose any rights to your occupational pension if you move to another country. The pension either stays invested in the Dutch fund or pays out once you reach pension age.

Transfers abroad are sometimes possible, but they can have tax consequences. It is often better to leave the pension in the Netherlands.

Your UPO pension statement

Every year, you receive a Uniform Pensioenoverzicht (UPO) for your occupational pension. This is a statement that shows:

- the pension you have built up

- the pension you are expected to receive

- what happens in case of disability

- what your partner may receive if you die

It is very wise to save your UPO statements. If you ever leave the Netherlands, these documents make your future pension administration much easier.

Pillar 3: Private and voluntary pensions

This pillar is where you can add flexibility and security to your already existing pension scheme(s). Private pension options include:

- lijfrente (annuity products)

- private pension accounts

- long-term investment products

- tax-advantaged pension savings

People usually choose these plans to cover gaps, add extra retirement savings, or benefit from tax incentives. We recommend Brand New Day, a supplementary pension that is very well-suited for expats in the Netherlands.

Why internationals often need a private pension

If you:

- arrive in the Netherlands later in life

- plan to stay only temporarily

- work for an employer without a pension plan

- are self-employed

then a private pension is extremely useful, as the Dutch state pension (AOW) and many employer schemes won’t fully cover your retirement needs.

In these situations, a private pension gives you control and the chance to make up for missing or limited pension accrual in the Dutch system.

Example scenario 3: arriving later in life

Let’s say you move to the Netherlands at 50 and stay until retirement. You build up about 34% AOW plus any employer pension. Because your AOW will be quite low, many internationals in this situation choose to set up private pension savings to fill the gap.

Pension options for freelancers (ZZP’ers)

Freelancers in the Netherlands do not automatically build up an occupational pension via an employer. They still accrue the state pension (AOW), but any extra pension on top of that is their own responsibility.

To make up for this, many ZZP’ers set up their own long-term investment accounts, sometimes with tax benefits.

You can also look into annuity products or other private arrangements. Because the responsibility lies entirely with you, it is worth researching early.

Example scenario 4: freelancing in the Netherlands

You work as a ZZP’er for seven years. You build about 14% AOW, but you do not get an employer pension. Without arranging a private pension or investment plan yourself, your retirement income will be very limited.

How to check your pension in the Netherlands

The most helpful tool in the whole Dutch pension universe is mijnpensioenoverzicht.nl. This national platform shows your complete pension picture in one place.

It includes:

- your AOW accrual

- your occupational pensions

- estimated future income after retirement

- estimated partner benefits

You simply log in with your DigiD and get access to everything.

Pro tip: If you ever leave the Netherlands, download your full pension report. It makes international retirement planning much easier later on.

How are Dutch pensions taxed?

Pension income in the Netherlands is treated the same way as regular income, which means it is taxed in Box 1 once you start receiving it. The exact amount depends on your total pension income and whether you live in the Netherlands or abroad at the time.

If you retire in the Netherlands, your AOW and occupational pensions are taxed under the lower “pension” tax brackets for seniors.

If you retire outside the Netherlands, tax treaties determine where you pay tax and how much. Some countries tax Dutch pensions locally, while others allow the Netherlands to tax first.

Private pension products, like lijfrente, also follow specific tax rules. You usually receive a tax benefit while saving, and then pay tax on the payout later.

It is not the most thrilling part of retirement, but it is worth checking how your future income will be taxed before you make long-term plans.

What’s changing for the Dutch pension system

Like many other countries, the Netherlands is currently in the process of shifting to a new pension system.

The so-called Future Pensions Act is the biggest pension reform in decades.

Why is the system changing?

The old pension system relied heavily on collective formulas that worked well decades ago but did not align with modern careers. People change jobs more often, work flexibly, or switch sectors, and the old rules sometimes create imbalances between age groups.

The new pension system aims to fix this. It is:

- more transparent, so you can actually see how much of your pension is yours

- more personalised, with growth that better reflects your own contributions

- more linked to real investment returns, instead of slow, collective smoothing

- fairer for younger and older workers, so gains and risks are shared more evenly

In other words, the system shifts from a “one size fits all” approach to one that follows your individual pension pot more closely.

What the reforms mean for you

Your pension fund may switch to a new structure over the next few years. You might see:

- changes in how your money is invested

- clearer personal pension pots

- slightly more fluctuation in expected payouts

- updated communication from your pension fund

The transition is gradual and varies by fund.

You usually don’t need to take action yourself, but do read messages from your pension fund carefully — in some schemes you may be asked to choose or confirm certain options during the transition.

What you can do now to prepare for retirement in the Netherlands

Even if retirement feels far away, a little planning helps.

READ MORE | 11 money-saving hacks for life in the Netherlands

Here is a simple checklist:

- Log in to mijnpensioenoverzicht once a year

- Save your UPO statements and payslips

- Ask your employer how your pension is arranged

- Consider a private pension if you expect gaps

- Track your total years in the Netherlands for AOW

- Keep your DigiD updated

- Read any messages from your pension fund

You do not need to become a pension expert, but having a general overview now will save a lot of confusion in twenty or thirty years.

Dutch pension vocabulary explained

| Term | Meaning |

| AOW | The Dutch state pension. |

| SVB | The organisation that pays AOW. |

| Pensioenfonds | A collective pension fund. |

| Lijfrente | A private annuity pension product. |

| UPO | Annual pension statement. |

| Jaarruimte | Your tax-free pension saving allowance per year. |

| Reserveringsruimte | Extra catch-up allowance for pension savings. |

| Pensioenpremie | The contribution paid into your pension. |

The Dutch pension system may seem confusing at first, but it is built to provide a stable foundation for life after work.

Retirement might still be far away, but your future self will be grateful that you took the time to understand things today.

Do you have any questions about Dutch pensions? Leave them in the comments!

Do I lose my pension if I leave the Netherlands?

No. You keep your AOW percentage and your occupational pensions. These will be paid out wherever you live, although tax rules may vary.

Can I retire in the Netherlands as a foreigner?

Yes, but non-EU nationals may need to meet income requirements to maintain long-term residency. Your pension income can help with this.

What happens if I worked in more than one country?

Within the EU, pension rights are coordinated. Each country pays its portion once you reach retirement age. Outside the EU, it depends on bilateral agreements.

How much pension will I receive?

Your retirement income depends on:

- your investment returns

- how long you lived in the Netherlands

- what your employer paid into your pension fund

- what you saved privately

Do I need to apply for my pension?

If you live in the Netherlands, AOW starts automatically once you reach your AOW age. If you live abroad, you must apply through the SVB.

Occupational and private pensions require applications once you reach retirement age.

Are Dutch pensions taxed?

Yes. Dutch pension income is taxed as income, although the rate depends on your residency. If you live abroad, tax treaties determine who collects the tax.

What if I lose my DigiD before retiring?

You can request a new DigiD abroad, but it might take some time. Better to download and save all pension records early.

Will my partner receive a benefit when I die?

Many occupational pensions include survivor benefits. Always check your fund rules.

Hello,

I am looking for information about my possible situation in the future. I have been here for 5 years as knowledge migrant. I plan to work until retiremt. I am also considering either having a pr or going for naturalization.

And later go back to stay outside NL in a non-Eu country.

Can I receive the my pension outside NL?

Is a pensioner required to go back to NL after a specified no. of months or years to continuously receive his pension?

Hi Dindo,

Whether you can receive Dutch state benefits (AOW) depends on whether the country you plan to retire in has a social security treaty with the Netherlands. In many countries it is possible, but not in all. You can check the situation for your country on the website of the AOW administrator: https://cutt.ly/cgQj0rY

If you would like to know more, we have just launched a website to help expats and knowledge migrants like you understand your Dutch pension. Have a look at https://myDutchPension.nl to learn more.

Best,

Jan

Hi i worked in holland for 4 years how do i claim my pension as i am 63. When i left Breda they told me that they would get intouch but i have heard nothing can yoj help me

Thank you

Hi – I am taxed both payroll tax and health insurance on my private Dutch pension. Do I have to pay this as a I live in the UK? Thanks

I am an Australian citizen and resident. I have a company pension from Fokker. Do I have to pay Dutch Tax on my pension?

Hi, I lived and worked in the Netherlands for ten years, I am a UK citizen and have returned to the UK. Can I and how can I claim my NL (AOW) pension.

Hi Chris! Hope that this information from the Dutch government website can help you with this! https://www.netherlandsworldwide.nl/aow-pension-abroad/what-is-aow.

This page is specifically for getting AOW pension when living outside of the Netherlands: https://www.netherlandsworldwide.nl/aow-pension-abroad/how-to-apply.

Hope it helps!

Hello,

I am a US citizen living in California but would like to immigrate to the Netherlands when I retire. I will have a pension (not just social security) from my employer. Would this be possible?

Hi/Hoi, I am a British Citizen living for 17&1/2 years in The Netherlands. Due to retire in couple of years. I am entitled to full UK State Pension. How will that UK State pension be treated tax wise in The Netherlands. I will also receive AOW for 19 years residency in The Netherlands.

alvast bedankt