So you’ve built up some capital, and now you’re asking yourself the big question: should I save or invest my money in the Netherlands?

It’s a common crossroads, with interest rates jumping around, inflation pushing your grocery bill higher, and Box 3 continuing to confuse both internationals and lifelong Dutchies.

The good news? You don’t need a finance degree to figure out what to do. Your choice depends on a few simple things: how long you plan to keep the money untouched, how comfortable you are with risk, and how long you think you’ll stay in the Netherlands.

Let’s walk through it.

This post might have affiliate links that help us write the articles you love, at no extra cost to you. Read our statement.

Investing in the Netherlands

We all know how saving works, so let’s start with the more intimidating (and exciting) option: investing your money.

In fact, data suggests that nearly every Dutch household saves, but investing is a different story. Just a quarter of households invest — and the top 10% now control over half the country’s wealth.

That gap says a lot.

How investing in the Netherlands works for residents and expats

Most internationals can invest in the Netherlands without any issue. You’ll find a few popular paths:

-

ETFs or Exchange-Traded Funds (groups of investments such as stocks, bonds, or commodities that trade on a stock exchange)

-

Index funds

-

Robo-investing

-

DIY stock investing

Many people start with ETFs because they’re simple and diversified. If the idea of choosing individual companies terrifies you (fair), ETFs remove the guesswork.

Pros and cons of investing

Investing is a rollercoaster, where things are calm one month and dramatic the next. But over many years, markets trend upward, and that’s where the power lies.

✅ Pros:

- Higher long-term growth

- Helps protect your money from inflation

- Compound interest allows your gains to grow further

❌ Cons:

- Short-term losses are normal

- Requires patience

- Panic or emotional decisions can sabotage progress

Dutch investment taxation (Box 3)

Before you get too far into investing, it helps to understand how the Netherlands taxes your assets.

Investments fall under Box 3, which uses an assumed return rather than your actual gains. The system works with a few “fictional” return bands, and investments are assigned a higher assumed return than cash-like assets.

This means you may be placed in a higher band if you hold significant investments. That sounds harsh, but here’s the important bit: long-term investment growth often beats both inflation and the Box 3 assumptions, so many investors still come out ahead over time.

How safe are investments in the Netherlands?

Investing doesn’t come with the same guarantee that savings do, but it isn’t a free-for-all either.

Dutch brokers follow strict rules set by the AFM (Authority for the Financial Markets). Many platforms also keep client assets in separate legal entities, so even if a company disappears, your investments don’t vanish with it.

READ MORE | Best crypto exchanges in the Netherlands [2026 guide]

It’s not absolute safety, but it’s a well-controlled environment.

Let op, internationals: if you move countries, your broker may not let you keep your account. Several platforms require you to close your account the moment your tax residency changes, so it’s worth checking before you commit.

Best investment platforms in the Netherlands

Your investment platform matters more than you might expect. Fees vary, apps differ, and some brokers feel like a friendly guide while others feel like a hectic aircraft cockpit.

Trade Republic: simple app with fractional investing

Trade Republic is one of the most user-friendly options out there. The app is clean, easy, and quick to get used to.

You can also buy fractional shares (meaning you don’t need €300 to buy a €300 stock), and the fees are minimal. It’s ideal for beginners who want a smooth, modern experience.

DEGIRO: low fees and a broad ETF selection

DEGIRO is a favourite among internationals because it keeps costs affordable and offers access to a huge list of ETFs.

It’s perfect if you want to invest regularly without feeling like fees are eating half your returns. The interface is straightforward, though slightly more “finance-y” than other platforms.

Disclaimer: Investing involves risk of loss.

Scalable Capital: automated plans and recurring investments

Scalable Capital shines if you love automation. You can set up recurring monthly ETF investments, choose from flexible or “Prime” plans, and let the platform handle most of the work.

It’s especially good for people who want consistency but don’t want to manage every buy button themselves.

These options are beginner-friendly, inexpensive, and reliable for building long-term portfolios.

Saving for retirement, instead? A popular Dutch option is Brand New Day, which allows you to invest monthly in pension funds and offers tax benefits if you meet the conditions.

READ MORE | You should be supplementing your Dutch pension: here’s why (and how to do it)

It’s especially handy if your employer pension feels underwhelming and you want to build an extra layer yourself.

What to check before choosing an investment platform

A quick checklist:

-

Costs (fund fees + broker fees)

-

App experience (is it pleasant or painful?)

-

Customer support

-

Whether they allow foreign addresses

-

Safety structure

-

Extra features (automatic investing, fractional shares, Crypto, etc.)

However, your first platform doesn’t need to be your last, and it’s wise to review your setup once a year.

Saving money in the Netherlands

Now let’s look at the more predictable option.

Saving is extremely common here, with a whopping 95% of Dutch households opting to save, even if it’s just small amounts each month.

It fits the Dutch preference for stability and being prepared for whatever chaos life throws at you (a.k.a. stolen bicycles or appliances breaking at the worst time).

How Dutch savings accounts work

Savings accounts with Dutch banks are simple and highly secure, and they work pretty much like elsewhere in the world:

-

You earn interest

-

You can access your money whenever you want

-

Deposits up to €100,000 per bank are protected by the EU’s Deposit Guarantee Scheme

That guarantee alone is enough to make many people stick with saving rather than investing.

Pros and cons of saving

Savings give you stability, but not much growth.

✅ Pros:

- Safe and predictable

- Perfect for emergencies

- No market swings

❌ Cons:

- Low long-term returns

- Inflation slowly reduces the value

- Not ideal for wealth-building

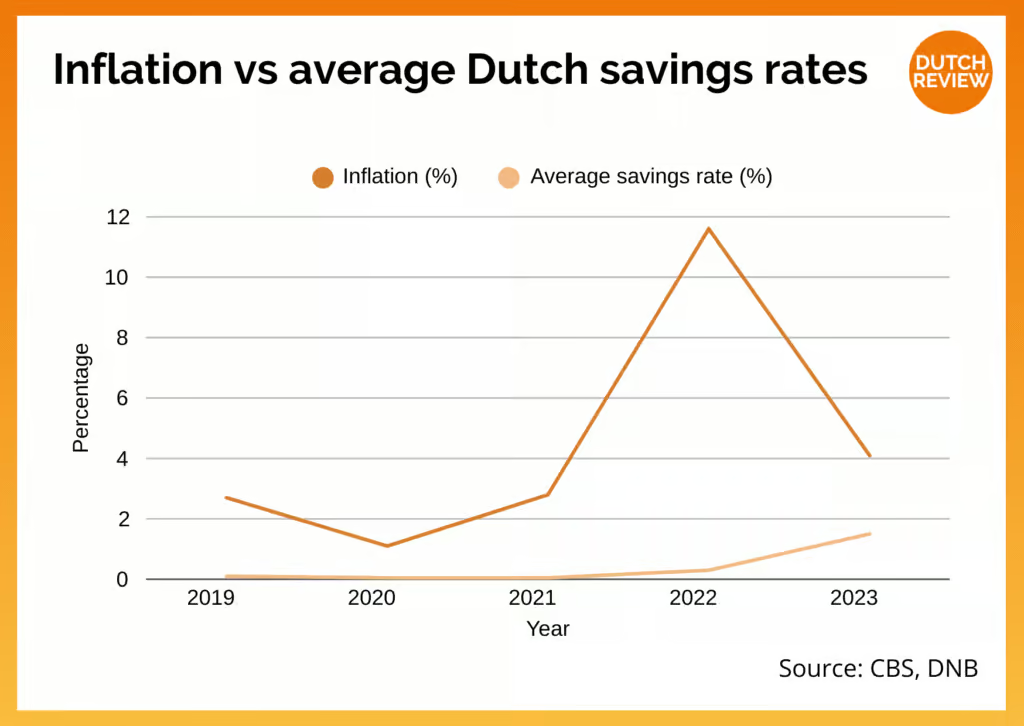

Dutch savings interest rates

Savings rates in the Netherlands vary, but generally, you can expect:

-

1% to 1.7% at most major Dutch banks

-

Higher rates from online banks or platforms like Raisin

Inflation often exceeds these rates. Even as your account balance increases, the amount you can buy may decrease.

Taxes on savings (Box 3)

Savings are also taxed under Box 3 using assumed returns. Smaller balances aren’t hit very hard. Larger balances may face higher deemed-return percentages. It’s worth understanding once you move from “starter savings” to larger amounts.

Best savings accounts in the Netherlands

Not all savings accounts are created equal. Some banks offer convenience. Others offer much better interest rates. Choosing the right one makes a real difference.

bunq: feature-rich, modern banking

Dutch neobank bunq is popular among internationals because it’s fast, modern, and very user-friendly. You can open multiple “pots,” set up automated saving, and track spending with playful visuals.

With a 3.01% interest rate, its savings rate is higher than that of traditional banks, and the app experience is one of the best in the Netherlands.

Trade Republic: best high-yield savings account

At 3%, Trade Republic offers one of the highest flexible savings rates available in the Dutch market, especially compared to big traditional banks.

Money is held in partner banks within the EU’s deposit guarantee system, and interest is paid monthly — a big plus if you like watching your balance tick upward.

Raisin marketplace: highest-rate savings rates across Europe

Raisin isn’t a bank itself but a platform that gives you access to dozens of EU banks with far higher interest rates than Dutch banks typically offer.

With rates up to 2.85%, you can always switch accounts when better rates appear, and everything stays under the €100,000 EU deposit guarantee per bank. It’s ideal if your priority is the best return rather than the prettiest app.

READ MORE | Best fixed-term deposit savings accounts in the Netherlands in July 2026

What to check before choosing a savings account

-

Interest rate

-

Withdrawal limits (if any)

-

App and website usability

-

Deposit guarantee eligibility

-

Transfer speed

The best savings account is the one you actually use consistently and review annually.

Saving vs investing in the Netherlands: which is better?

You guessed it, there’s no single, definitive answer, but here’s the general rule:

-

Saving protects your money.

-

Investing grows your money.

Both have their place, but they do different jobs.

Liquidity, risk, and returns

| Category | Saving | Investing |

| Liquidity | High | Medium |

| Risk | Low | Medium to high |

| Expected returns | Low | Higher |

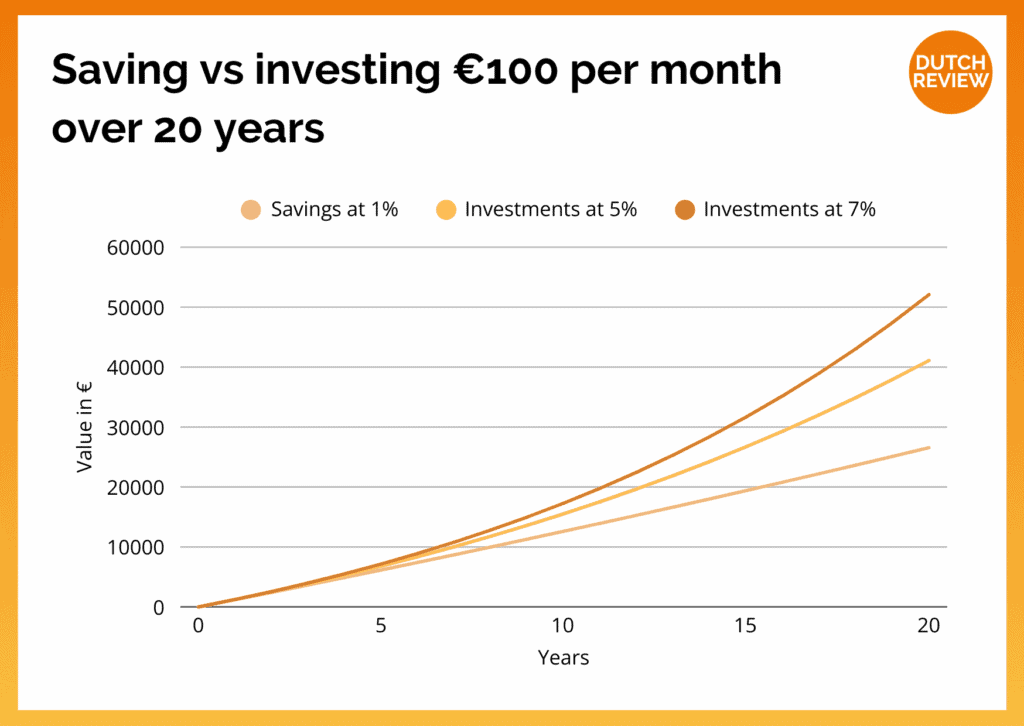

Example: saving vs investing €100 per month

If you save €100 a month for 20 years at a 1% interest rate, you’ll end up with about €26,600.

If you invest €100 a month at a conservative average of 5% growth, you get around €41,000.

At 7% growth? Around €52,000.

Keep in mind that inflation may reduce the real value of savings, while investments generally outperform inflation over time.

When saving is the better choice

-

Short-term goals (holidays, emergency fund)

-

Expected big expenses in the next 2–3 years

-

Nervousness about risk

When investing is the better choice

-

Long-term goals

-

Retirement planning (Brand New Day is a common option for this)

-

Generating real growth

-

Beating inflation

For expats, long-term planning also depends on your future location, so think about how your pension and investments may be affected.

How to decide between saving and investing in the Netherlands

Choosing the “right” path depends on a few key factors.

-

Your time horizon: Short-term needs = saving, long-term goals = investing.

-

Your risk tolerance and financial stability: Are you okay with seeing your balance drop sometimes? If not, stick to saving. If you can ride out market bumps, investing works in your favour.

-

Your goals as an expat in the Netherlands: Will you stay here long-term? Do you plan to transfer money back home? Do you have multiple tax systems in your life?

If you plan to stay for years, investing becomes a practical tool. If your life is more temporary, saving may suit you better for now.

Saving is safe, while investing builds wealth. Most internationals benefit from doing a bit of both.

You can start by building a comfortable emergency fund. Once that’s sorted, investing becomes a practical way to grow your money over the long term.

Your situation will change as your life in the Netherlands evolves. Review your setup periodically, adjust as needed, and keep moving forward.

Do you have any tips on saving and investing in the Netherlands? Leave them in the comments!

Saving vs investing in the Netherlands: Frequently asked questions

Is it better to save or invest in the Netherlands in 2026?

It depends on your goals. If you need the money soon, save. If you’re planning five years or more ahead, investing usually wins.

How much should I keep in savings?

A good starting point is a few months of living costs, a.k.a. enough to handle surprises without panic.

Can internationals invest easily in the Netherlands?

Yes. Most brokers accept expats, and internationals commonly use platforms like DEGIRO, Trade Republic, and Scalable Capital.

Is now a good time to invest or save?

Saving is always smart for short-term needs. For investing, time in the market matters more than perfectly timing it — regular contributions typically work best.

Do I pay different tax rates on savings and investments?

Sort of. Both fall under Box 3, but investments get a higher “assumed return” than savings. In practice, long-term returns often make up for that.

Can I invest for retirement as an expat?

Yes, though it depends on how long you stay in the Netherlands. Many people use supplementary pensions like Brand New Day for long-term pension investing, but the money is locked until retirement age.

What if I move countries later?

Some brokers let you keep your account, while others don’t. It’s worth checking before you start investing heavily.